If you’re aiming to buy in Huntsville or Madison in the next 6–18 months, the question isn’t just “how much do I need?”—it’s “how do I get there without pausing life?” Here’s a simple, realistic plan I share with first-time buyers and relocators.

Step 1: Set a target that matches local reality

Start with a price band that fits your commute and lifestyle—then back into the cash you’ll need:

-

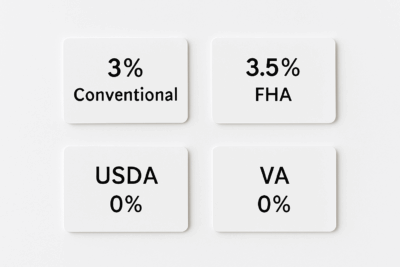

Down payment: can be as low as 3% on many conventional loans for qualified first-time buyers (Freddie Mac Home Possible/HomeOne). (Freddie Mac)

-

FHA: minimum 3.5% down for qualified borrowers (with mortgage insurance). (consumerfinance.gov)

-

USDA (eligible rural areas like parts of Limestone/Madison counties): 0% down for eligible buyers. (Rural Development)

-

VA (active-duty, veterans, some surviving spouses): often no down payment required. (Veterans Affairs)

You’ll also plan for closing costs (roughly 2–5% of the loan)—and we’ll try to offset a chunk of that with seller credits or builder incentives when possible. (Yes, we’ll model it both ways.)

Step 2: Use assistance that actually moves the needle (Alabama-specific)

If you’re close but not quite there, down payment assistance can bridge the gap. In Alabama, the AHFA “Step Up” program pairs competitive rates with assistance funds toward down payment/closing costs for eligible buyers. We’ll check qualification, income limits, and participating lenders together. (AHFA)

Step 3: Automate the savings (and protect your momentum)

Set up an auto-transfer from checking to a separate “Home” account every payday. Behaviorally, it works better than “I’ll move it later,” and it keeps your progress visible. This habit-first approach is consistent with mainstream personal-finance guidance highlighted by Real Simple’s experts. (Real Simple)

Set up an auto-transfer from checking to a separate “Home” account every payday. Behaviorally, it works better than “I’ll move it later,” and it keeps your progress visible. This habit-first approach is consistent with mainstream personal-finance guidance highlighted by Real Simple’s experts. (Real Simple)

Where to park it: keep near-term home funds safe and liquid—think high-yield savings or CDs if your timeline is under five years (not the stock market). (Real Simple)

Step 4: Make 2–3 easy wins add up

-

Kill lifestyle creep: Cap dining/retail categories for a season and redirect the difference to your Home account. (Small trades, big runway.) (Real Simple)

-

Snowball high-interest debt: Lower balances → better credit tiers → better rates when you apply. (Real Simple)

-

Turn skills into cash: A short-term side gig can accelerate savings without touching your core routine. (Real Simple)

Step 5: Choose the loan lane that fits you

Here’s the quick, practical way we’ll compare options:

-

Conventional 3%: great for strong credit and modest down payment; PMI until ~20% equity. (Freddie Mac)

-

FHA 3.5%: more flexible on credit; includes upfront/annual mortgage insurance—sometimes the cheapest path if your score is rebuilding. (consumerfinance.gov)

-

USDA 0%: income/area eligibility applies; terrific for certain Athens/Limestone pockets. (Rural Development)

-

VA 0%: often lower rates + no PMI for those with VA benefits. (Veterans Affairs)

We’ll run side-by-side payment scenarios (price cut vs. seller credit vs. buydown) so you can pick the path that wins on monthly comfort—not just sticker price.

Step 6: Use “found money” to jump ahead

Tax refunds, bonuses, and gifted funds (properly documented) can count toward closing or down payment on many programs. I’ll coordinate with your lender so the paper trail is clean and your approval stays on track. Guidance to use windfalls for home goals rather than lifestyle upgrades is echoed by personal-finance pros. (Real Simple)

What this looks like in Huntsville/Madison

-

Timeline: Most buyers I coach hit a realistic savings goal in 4–12 months once we automate and pair it with the right loan lane.

-

Neighborhoods to watch: Payment-friendly pockets in Meridianville, Monrovia/Harvest, and parts of Athens/Limestone—plus targeted new-construction incentives we can leverage for credits or temporary buydowns.

John’s actual MLS Listing – 43 Pine Street, Huntsville, AL

Quick checklist (save this)

-

☐ Pick a price band and confirm loan lane (Conventional 3%, FHA 3.5%, USDA/VA 0%).

-

☐ Automate transfers to a separate “Home” account; keep funds in HYSA/CDs. (Real Simple)

-

☐ Apply for AHFA Step Up if eligible. (AHFA)

-

☐ Kill 1–2 spending leaks; put windfalls toward the fund. (Real Simple)

-

☐ Ask me for a lender intro + a payment-first plan (with credits/buydowns modeled).

Ready to map your payment?

Buying in Huntsville, Madison, or anywhere from Athens to New Market Alabama area? Reach out at 256-797-2283. I’ll show you where the value is, where the growth is heading, and which homes line up with your long-term goals.

Friend, contact me because as a top real estate agent in the Huntsville area—born and raised here, and still helping families find their way home, I am the Agent you need on your side.

The Brooks Family of REALTORS® has served our community since 1972. Let’s make your move a smart one.

Written by John Wesley Brooks,Top Realtor®️ with Capstone Realty, serving North Alabama.

Contact: 256-797-2283 | [email protected] | www.johnwesleybrooksrealestate.com

Find me Here: Google Business Profile | Facebook | Instagram | LinkedIn | Twitter | YouTube | Realtor.com | Zillow

👉 Read more about John’s tips and advice to maximize savings before buying a home, here.